⚡ AI, Data Centers, and the Growing Strain on Power Systems

- The Rise of AI and Data Center Electricity Demand

AI and data centers have become global focal points—dominating headlines and reshaping energy demand forecasts. Powering these facilities, especially those supporting AI workloads, requires vast amounts of electricity. According to the Energy and AI report by the International Energy Agency (IEA), global investment in data centers nearly doubled between 2022 and 2024. Hyperscale data centers, often exceeding 100,000 square feet and sometimes reaching up to 1 million square feet, are among the most energy-intensive.

The IEA projects that electricity consumption from AI infrastructure will rise sharply—from 415 terawatt-hours (TWh) in 2024 to 945 TWh by 2030. A significant share of this growth is expected to come from the U.S. AI sector. Multiple sources forecast that U.S. electricity demand driven by data centers and AI will grow at an atypically high rate of 1.5% to 2.2% annually through 2050.

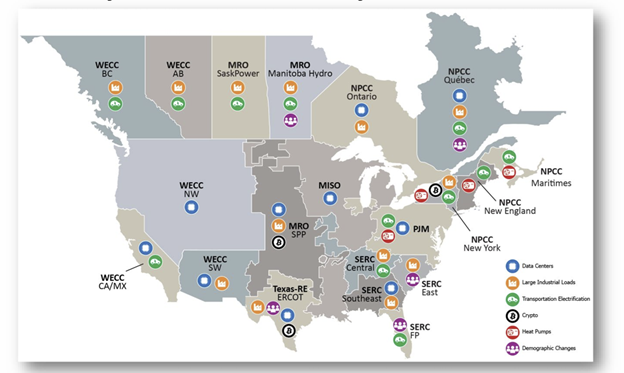

(See Figure 1 for a reproduction of NERC’s primary demand drivers.)

Figure 1: Primary Demand Drivers by NERC

Source: Long-term Regional Assessment, North American Electric Reliability Corporation (NERC)

Source: Long-term Regional Assessment, North American Electric Reliability Corporation (NERC)

- Data Center Load Profiles and Grid Reliability

To assess the impact of data centers on electric systems, it is essential to understand their consumption patterns. Unlike residential or commercial loads, data centers operate continuously—consuming electricity 24/7. This constant demand cannot be met reliably by intermittent renewables alone. Solar and wind generation fluctuate with weather and time of day, requiring system operators to maintain backup or fast-response power sources.

To meet clean energy goals, hyperscale operators like Microsoft, Meta, Google, and Amazon have secured long-term power purchase agreements (PPAs) for 24/7 firm energy. These PPAs often bundle renewables, battery energy storage, and wholesale spot market purchases. However, this raises a critical question:

Can wholesale spot markets sustainably absorb incremental demand without compromising reliability?

- The Duck Curve and Grid Flexibility Challenges

The California Independent System Operator (CAISO) and the Electric Reliability Council of Texas (ERCOT) have both experienced a mismatch between solar generation and electricity demand—illustrated by the “Duck Curve.” First introduced by CAISO, the curve shows low net demand during midday solar peaks and steep ramp-ups in the evening as solar output declines.

In response, various RTOs/ISOs have developed new market products to enhance grid flexibility and integrate renewables more effectively. These include fast-ramping resources, demand response programs, and energy storage solutions.

- Reliability Risks and Market Signals

As data center and AI-related electricity demand surges, power systems are struggling to keep pace. According to NERC’s 2025 Summer Reliability Assessment, six of seven RTOs/ISOs face elevated risks of insufficient operating reserves during above-normal conditions. This has triggered debates around resource adequacy and even proposals to redesign capacity markets.

Wholesale markets like PJM and MISO are experiencing tightening supply conditions due to load growth, interconnection backlogs, and generation retirements. These pressures are reflected in rising capacity prices:

- MISO’s Summer 2025 capacity auction cleared at $666.50/MW-day, with a 40% reduction in surplus capacity.

- PJM’s 2026/2027 auction saw a 22% increase in RTO-wide clearing prices, reaching $329.17/MW-day, with some local zones exceeding $440/MW-day.[³]

Even with 2,669 MW of new capacity additions and 1,100 MW of withdrawn deactivations, PJM expects a 5,400 MW demand increase—primarily driven by data centers. PJM’s Independent Market Monitor (IMM) advised FERC that data centers should procure their own power resources.[⁴]

- Behind-the-Meter Strategies and Infrastructure Implications

Many data centers are doing just that—securing long-term PPAs with stable baseload sources such as nuclear and natural gas. Some utilities and independent power producers (IPPs) have signed deals to restart previously retired nuclear plants, bypassing lengthy interconnection queues.[⁶] Others are investing in advanced nuclear technologies, including Generation IV and small modular reactors (SMRs). For example: Alphabet Inc. (Google) signed PPAs with Oklo and Kairos Power for advanced nuclear projects.[⁷] Some developers have opted for natural gas instead. For example, Essential Utilities plans to invest $26 million in a 1,400-acre data center in Greene County, Pennsylvania, powered by 944 MW of behind-the-meter natural gas combined cycle turbines, backed by battery storage and grid interconnection.[⁸] Dominion Energy received approval from the Virginia Public Utilities Commission (VPUC) to build new fossil-fueled plants, including a 944-MW natural gas peaking complex to meet surging demand.[⁹][¹⁰] Opponents in the case has argued for alternatives such as batteries, virtual power plants, and distributed generation to reduce grid integration costs.

- Transmission and Cost Allocation Challenges

Power plants serving data centers are often located behind the transmission grid—known as “Behind-the-Meter” (BTM). While these facilities may appear off-grid, they are not fully isolated. Any BTM facility can push or pull electrons, affecting transmission operations and neighboring generators.

This raises complex questions about cost allocation and tariff design. Should data centers be classified as network customers or point-to-point transmission customers? If classified as network customers, would their reliability costs be socialized across the grid?

Existing transmission tariffs may not adequately capture the services provided to BTM data centers, including ancillary services. As data center growth accelerates, regulators and market operators must revisit these frameworks to ensure fairness, reliability, and cost transparency.

Footnotes

[1] IEA Energy and AI Report, 2024[2] NERC 2025 Summer Reliability Assessment

[3] PJM and MISO Capacity Auction Results, 2025–2027

[4] IMM Statement to FERC, 2025

[5] Utility PPA Announcements, 2024–2025

[6] DOE Interconnection Queue Analysis, 2025

[7] Google PPAs with Oklo and Kairos Power, 2025

[8] Essential Utilities to Invest $26MM in Pennsylvania Data Center Hart Energy (https://www.hartenergy.com/exclusives/essential-utilities-invest-26mm-pennsylvania-data-center-213948) [9] Dominion Energy Fossil Plant Approval, VPUC, July 2025; VPUC Reliability Center Filing, August 2025

[10] Virginia Decarbonization Law Exception Request, 2025